While I don’t normally write exclusively about paper assets, I see a coming disaster involving shareholders and bondholders that I feel compelled to talk about. In my opinion, there is a dangerous situation evolving in the U.S. and global capital markets that is obvious once it is pointed out. And yet, I have not seen a single article in the mainstream financial press discuss this topic. I hope to do my part to address this deficiency.

But before I can describe my worries, we need to have an intimate understanding of corporate capital structures. Many average people who invest in the stock market in their retirement accounts do not understand the importance of a company’s capital structure. The capital structure is the way that a company finances itself. More specifically, it is the breakdown between the different tiers of financing that a corporation uses to fund its operations.

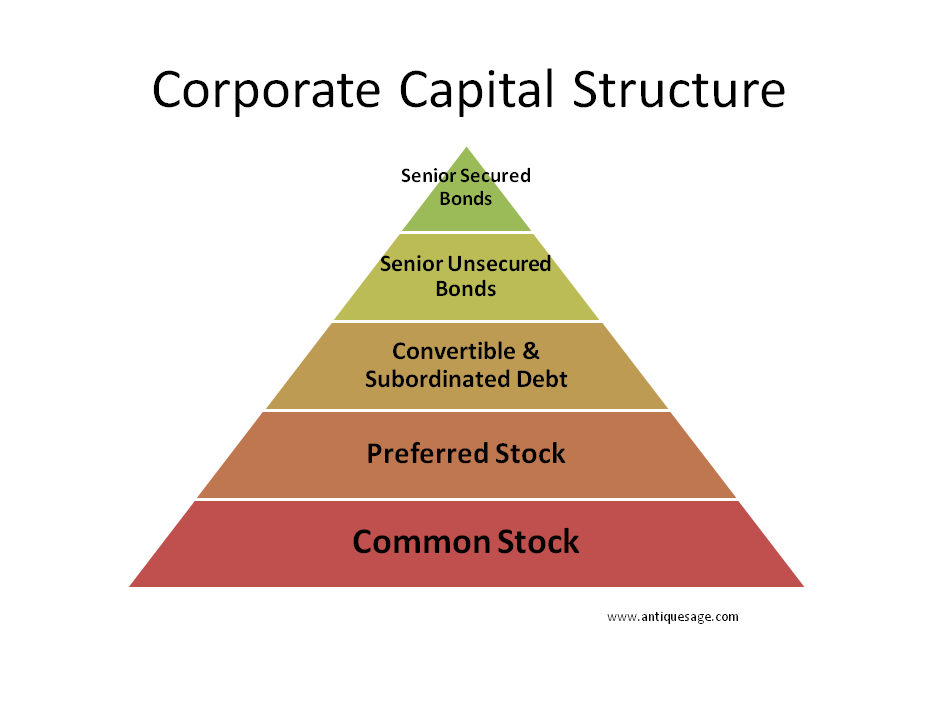

The most secured part of a company’s capital structure is composed of senior secured bonds. Senior secured bonds are corporate debt that has specific property pledged as collateral. This collateral can be anything from office buildings to factories to oil pipelines – any tangible property with a market value will work. Senior secured bondholders face little risk of loss in a bankruptcy due to the pledged collateral.

Next in a corporation’s capital structure are senior unsecured bonds. These debt instruments are very similar to senior secured bonds, except that they have no specific collateral pledged against them. This means that in a bankruptcy senior secured bondholders take their collateral first, leaving senior unsecured bondholders with whatever corporate assets are leftover. In the event of bankruptcy, senior unsecured bondholders generally sustain losses that range from modest to significant.

Moving further down the capital structure we come to convertible and subordinated debt. These fixed income instruments are similar to unsecured debt, except that they sometimes contain provisions that allow a company to suspend interest payments if they have cashflow problems. Even so, convertible and subordinated bonds are contractual obligations of the issuing company. In bankruptcy proceedings though, convertible and subordinated debts are junior to senior unsecured debts. Bondholders holding this slice of a company’s capital structure usually face large losses in bankruptcy restructurings.

Going one rung further down the capital structure we come to preferred stock. Preferred stock is considered a “hybrid” security. This means it has both debt and equity characteristics simultaneously. Preferred stock usually has fixed, periodic dividend payments. But it is also counted as equity for the purposes of measuring corporate leverage. Preferred stock payments can generally be indefinitely suspended if a company runs into financial trouble.

Some preferred stock is “cumulative”, meaning any missed interest payments must be made to the preferred stockholders before dividends can be paid on common stock. However, most preferred stock is non-cumulative in nature. Preferred stockholders are usually wiped out in bankruptcy.

Common shareholders are at the very bottom of the corporate capital structure. Common shares, also called stocks or equity, pay a variable dividend that is completely at the discretion of a company’s board of directors. When business is good, a company might pay very enticing dividends that increase over time. However, when business goes bad, dividends can be quickly cut or even eliminated altogether. In a corporate bankruptcy, common shareholders inevitably lose everything.

As you can see, a company’s capital structure is a lot like a ladder. The higher up you are on the ladder, the more secure your investment is and the lower your chances for loss in the event of bankruptcy. The flipside of this is that only the bottom rung – common stock – has a claim on the excess cashflow generated by a successful company.

And here’s where the problem lies. For the last decade the stock market has done wonderfully. Shareholders have enjoyed strong returns with modest volatility. Much of this has been driven, either directly or indirectly, by the world’s central banks, which have acted in concert to suppress global interest rates.

Although many investors don’t realize it, companies have benefited dramatically from lower interest rates as well. First, many companies have been able to refinance their high interest bonds into low interest bonds. This has been bad for bondholders, but great for shareholders.

However, corporate executives and directors couldn’t keep their hands out of the honey pot. Instead of simply refinancing their existing debt, many corporations have used cheap and plentiful debt to lever up their balance sheets. They largely used this onetime financial windfall to A) buy back common shares on the open market; B) pay out dividends to common shareholders; or C) buy rival companies in an attempt to gain market dominance.

All of these debt financed corporate activities have been beneficial to shareholders in the short term. But, they risk the solvency of many of these companies in the long term. The numbers are sobering.

According to the U.S. Federal Reserve’s Z.1 report, total non-financial corporate bond and loan liabilities outstanding as of March 31st, 2017 were over $8.6 trillion. This number has increased by a staggering 2.8 trillion dollars – almost 50% – over the course of the last 10 years. This is particularly telling because many financial pundits have claimed that U.S. balance sheets deleveraged substantially since the Great Recession.

But the numbers don’t lie. U.S. Corporate leverage is higher than it has ever been before. And overseas companies have largely engaged in the same destructive financial behavior as their U.S. counterparts.

Some people may point to healthy corporate cash balances as a mitigating factor in this situation. On the surface, this argument seems to have some merit. According to the U.S. Fed’s Z.1 report again, non-financial corporate cash is a robust 2.1 trillion dollars at March 31, 2017. In an attempt to be as lenient as possible about the definition of cash, I not only included traditional cash instruments in this amount – bank deposits, CDs, money market funds, repurchase agreements and commercial paper – but also longer dated “savings” vehicles companies sometimes use, like corporate bonds, municipal debt, agency bonds and treasury securities.

Over two trillion dollars of cash on corporate balance sheets sounds great, until you realize that those cash levels have only increased by $0.6 trillion over the last decade. This cash addition was completely swamped by the $2.8 trillion in debt these same companies have built up over the same period.

A Forbes article from 2016 makes those numbers look even more ominous. Most of that cash is held by only a handful of the largest and most successful U.S. multi-national corporations. According to the Forbes article, the 50 biggest cash hoarding U.S. non-financial companies held $1.14 trillion at December 31, 2015. This means that actual cash balances for the 4,000 odd remaining U.S. listed companies are collectively less than one trillion dollars. There goes the myth of cash-laden, rock-solid corporate balance sheets.

The consequences of this excessive corporate leverage have been repeatedly delayed. And, as long as the capital markets are happy to throw fistfuls of money at junk rated companies or anything that pays a dividend, not much will change. But everything in finance is cyclical, and all debt-fueled, corporate borrowing binges must eventually come to an end.

When that day finally comes, the place your investments hold in the corporate capital structure will matter a great deal. As cashflows shrink, companies naturally retrench. They spend less on advertising, R&D, mergers and employee wages and benefits. They also cut back, oftentimes dramatically, on the two things that tend to support share prices – stock buybacks and dividends.

If you hold common shares, which are the lowest rung of the capital structure, you will be disproportionately affected by these developments. Unlike interest payments to bondholders, corporations have no legal obligation to pay dividends to common shareholders and only very limited legal obligation to make payments to preferred shareholders.

As I like to put it, common stockholders hold the “business end” of the stick when it comes to the capital structure. What I mean by this statement is that while owners of common stock can potentially reap the greatest rewards if a company succeeds, they also simultaneously occupy the riskiest part of the corporate capital structure if anything goes wrong.

If the coming liquidity crisis is severe enough, there is a non-trivial chance for widespread bankruptcies in our over-levered corporate sector. Common and preferred shareholders would bear the brunt of the losses in this situation. In fact, it is normal for stockholders to have their shares cancelled outright in bankruptcy without any compensation.

Under these circumstances, a company’s bondholders are usually equitized, meaning all or part of their bonds are exchanged for new common stock in order to recapitalize the company, effectively making them the new owners of that company. The “haircut”, or loss, that bondholders take is proportional to the amount of assets the corporation has, its level of leverage and where the bonds stood in the old capital structure. The higher your bond in the capital structure of a company facing bankruptcy, the better. Shareholders almost always get nothing.

Even if an over-levered company isn’t forced to declare bankruptcy, it doesn’t mean that its common shareholders are free and clear. Many times, highly leveraged companies become zombie companies. This term was first popularized in Japan in the 1990s in the wake of its collapsed stock market bubble.

A zombie company is one that is kept on life-support by its lenders or bondholders. These lenders continue renewing loans to zombie companies to keep them out of bankruptcy when there is otherwise little hope of them paying down their debts. In return, a zombie company becomes the de facto property of the lenders. The lenders appoint representatives to the company’s board of directors and essentially have veto power over any major corporate decisions.

In addition, and perhaps most importantly for shareholders, effectively all future cashflows of a zombie company are redirected to the bondholders. The shareholders are owners of the company in name only, with few rights and no realistic hope for future financial gains. Dividends are almost always suspended in this situation, as well.

I suspect that when our current economic cycle finally turns, there will be widespread corporate bankruptcies. Many, many companies that do not declare bankruptcy will instead become zombie companies. Common and preferred shareholders will be all but wiped out by these developments. Instead, bondholders will usurp their privileges wholesale and effectively take ownership of a huge swath of corporate America. In the end, only bondholders will inherit the stock market.