To say that the future of Social Security is contentious is an understatement. We’ve been hearing for decades that the government entitlement program faces a looming cashflow crunch. Proponents of Social Security point to its gargantuan $2.9 trillion trust fund, while detractors say the trust fund is an accounting fiction.

And to be honest, for a long time I just didn’t care. For decades the system has simply kept humming along as if nothing was wrong. The sun rose in the east every morning, Social Security checks were direct-deposited like clockwork and life went on.

Then, out of sheer curiosity, I compiled historical and projected cashflow data on the pension program. I was shocked by what I discovered. This is the kind of information that you won’t find discussed by a panel of experts on CNBC or splashed across the front page of the Wall Street Journal.

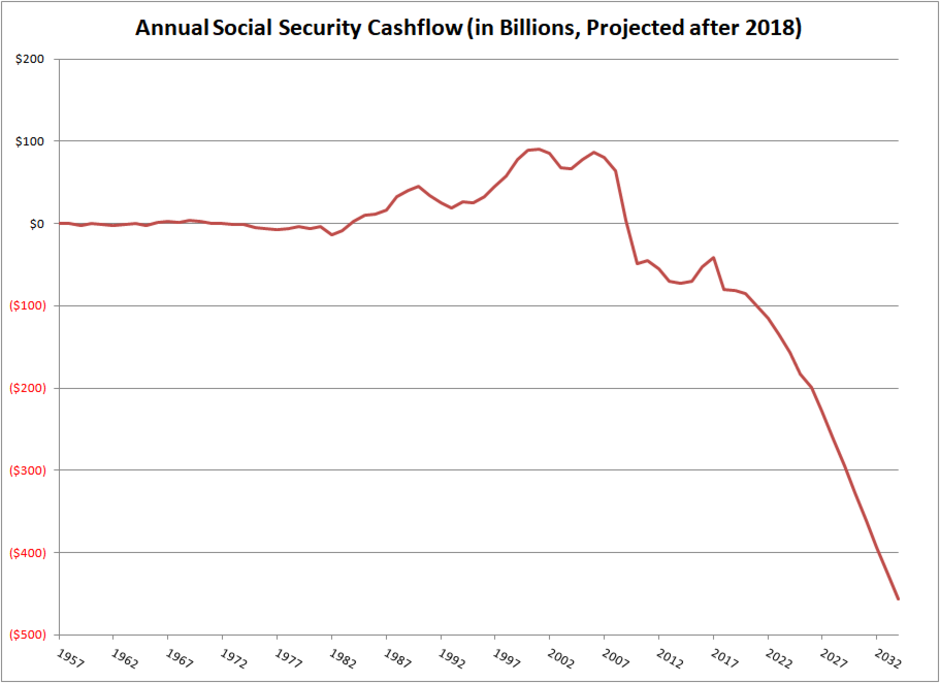

The chart at the top of this article shows annual Social Security cashflow for the historical period from 1957 to 2018, as well as the program’s projected cashflows from 2019 to 2034 (according to the Trustees’ 2019 Annual Report). It considers payroll taxes, income taxes on benefits and Federal reimbursements for payroll tax holidays (as occurred in 2011 and 2012) as positive cashflows to Social Security while benefit payments, administrative expenses and transfers to the Railroad Retirement Program are counted as negative cashflows.

You’ll notice that I’ve intentionally excluded the interest earned on the Trust Fund from the calculations. This is because any interest earned on the Trust Fund doesn’t change how the Federal government ultimately funds the program. When the time comes to payout benefits, the government must either do so from collected taxes or the proceeds of Treasury bonds sold to the public. Interest income and bond redemptions generated by the Social Security Trust Fund must be paid out of the government’s general fund – generally via the sale of an equivalent amount of Treasury securities to the wider public.

So for all the attention it gets, the Social Security Trust Fund really doesn’t matter very much. You could lop a zero off its $2.9 trillion balance sheet without changing the program’s funding requirements very much. Likewise, you could add a zero to the Trust Fund and get the same result. In the end, the money for benefits comes from current taxes and bond sales to the public, Trust Fund be damned.

This is all tediously academic…at least until you take a good look at the chart above. It shows how Social Security went cashflow negative in 2010 in the aftermath of the Great Recession, never to go cashflow positive again. For the last 10 years the entitlement system has been persistently cashflow negative – so much so that it is quite easy to dismiss as immaterial.

And I would agree with that assessment, up to a point. The annual Social Security cashflow deficits from 2010 until the present have been quite manageable, generally fluctuating between -$40 and -$80 billion in any given year. And the system will remain completely viable for a few more years in its current form. According to projections, the deficit will remain under -$100 billion through 2021.

But after that things start to get ugly. Social Security’s cashflow deficits will deteriorate from around -$100 billion in 2021 to -$400 billion in the early 2030s. As if that isn’t bad enough, the projections don’t take into account the possibility of an economic recession, which is a ridiculous assumption. If a recession were to occur anytime over the next 15 years, the situation would quickly go from dire to disastrous.

And a recession is coming, you can count on it.

This is why I find the Social Security Trustees’ projections that the Trust Fund will last until 2035 to be laughable. What will really happen is that we’ll most likely have a severe recession over the next few years which will accelerate all of the negative trends we see in the chart above. We’ll probably be seeing -$400 billion cashflow deficits in the program by the late 2020s and I find it reasonable to assume that the Trust Fund will be exhausted around the year 2030, give or take.

Now you may be wondering why I care when the Trust Fund runs out of money, considering I’ve openly stated that’s its size is immaterial. The answer is quite simple. The existence of the Trust Fund provides political cover for Congress to ignore the festering negative cashflow issue. Social Security is famously known as the third rail of American politics. Any politician who tampers with it gets permanently booted out of office, never to be re-elected again.

So the path of least resistance is to just ignore Social Security’s impending issues and pretend everything is alright. It is only once the Trust Fund is empty sometime between 2030 (in my estimation) and 2035 (according to the Social Security Trustees who assume no recessions) that ugly reality will stare us all in the face.

What does this mean for you and me?

If you are currently receiving Social Security payments, you are probably golden for the next 10 years. Even after that, there is a good chance you will be grandfathered into any reforms, meaning that you may well continue to get your checks on time and in the expected amount. Of course, this good news may seem like a Pyrrhic victory once you read what comes next.

If you aren’t old enough to draw on Social Security yet, then I suggest you start making other arrangements. The U.S. government is currently running a budget deficit of around -$1 trillion in 2019. This is a shockingly high number against the backdrop of a purported economic expansion. Thus far, negative Social Security cashflow has been a relatively minor part of this general budget deficit, contributing between 4% and 8% of the total.

However when the current Everything Bubble bursts and the economy inevitably enters a major recession, these numbers will deteriorate far more rapidly than most people expect. The Federal deficit will simply blow-out to -$2 to -$3 trillion per year, with Social Security making a significant (negative) contribution.

The only reasonable solution will be for the government to engage in money printing, aka helicopter money. In fact, academics have recently been attempting to rehabilitate the long-sullied reputation of money printing. Now they call it Modern Monetary Theory (MMT for short), claiming that it isn’t evil, just misunderstood. This is meant to fool the historically ignorant. But the results will be the same – the more money the government prints, the less value your existing dollars will have.

This is why I advocate that forward-looking individuals invest in tangible assets like antiques, bullion, fine art and gemstones. These hard assets can’t be printed at the whim of desperate central bankers or corrupt politicians. As a result, they will retain their value in a scenario where more traditional financial assets – like cash, stocks and bonds – crash and burn.

Read more thought-provoking Antique Sage investing articles here.

-or-

Read in-depth Antique Sage investment guides here.