There’s an old financial saying that you can’t time the market. And while I’ve found this dictum to be largely accurate, it does ignore one almost surefire way that investors can boost their investment results over the long haul.

I’m referring to allocating your portfolio based on broad valuation metrics. If you overweight asset classes that are undervalued while shunning those with overvalued, you simply can’t help but make money over long periods of time.

Perhaps the best way to do this is by forecasting real returns for asset classes. The word “real” in this context means returns that have been adjusted for inflation. For example, if you expect inflation to run at 2% per annum but your bond has a yield-to-maturity of 5%, then your real return is the difference between the two: 3%.

Now that 2020 is here, I thought it would be interesting to examine the major asset classes and project their real returns over the next decade.

The results are surprising, but not in a good way. Despite the 2019 stock market melt-up, investors in conventional assets have a whole lot of nothing to look forward to over the next 10 years.

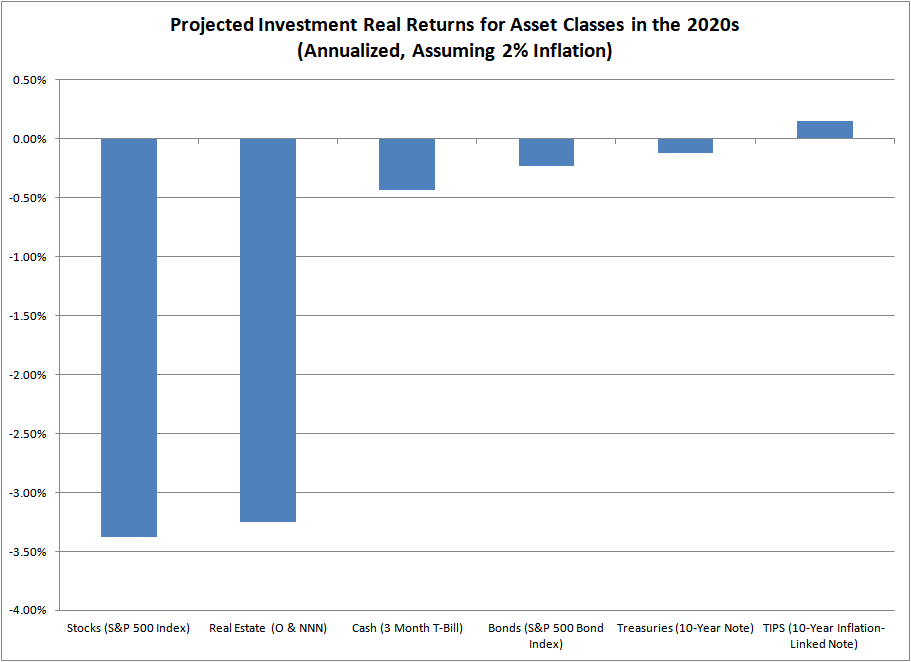

You can see this for yourself in the chart at the top of this article. It details my personal return projections across 6 popular asset classes between 2020 and 2030. These assets are: stocks, real estate, cash, corporate bonds, U.S. Treasury bonds and TIPS (U.S. Treasury inflation-protected bonds).

As an aside, my projections for stocks and real estate are based on a formula provided by the money manager John Hussman, founder of the Hussman Funds. You can read more about his methodology in an article I wrote back in 2017.

Now onto the crux of this article – the implications of my projected 2020s investment real returns.

First up are stocks, which are represented by the S&P 500 Index. The picture here is not pretty. According to my calculations, stocks are likely to decline by -3.38% in real terms every year during the 2020s. Ouch!

Of course, this estimate is just that – an estimate. If inflation or nominal GDP growth is different than my forecast (2.0% and 4.0% per annum, respectively), then the outcome will be different as well.

But the really big question mark regarding stocks is the multiple they trade at. At the end of 2019, the S&P 500 surpassed its highest price-to-sales multiple ever. Yes, higher than even the 1929 stock market peak or the 2000 Dot Com bubble.

Right now the index trades at 2.35 times sales, versus a more normal ratio of 1.0. In fact, if you discount the last 20 year period of market history (which has just been one long asset bubble train wreck), the average price-to-sales ratio is closer to 0.8. So I’m being quite generous by spotting the market a 1.0 multiple here.

In case you’re wondering, I use price-to-sales rather than price-to-earnings because earnings are much more volatile and easy to manipulate compared to revenue. And honestly, most other valid valuation measurements will give you similar results anyway, including price-to-tangible-book-value, Tobin’s Q ratio or market cap-to-GDP.

That last ratio, market cap-to-GDP is an interesting case. This valuation metric, which is favored by Warren Buffett, indicates that stocks (as represented by the Wilshire 5000 Index) will decline by a nominal 2.8% per annum over the coming years. Once you subtract the expected 2% inflation rate from this number, you end up with a dreadful -4.8% real return. This is actually worse than my already rather pessimistic stock market projections using the price-to-sales ratio!

Real estate is no safe haven either. I’ve averaged the valuations of two best-in-class REITs to represent this asset class: Reality Income Corp. (ticker “O”) and National Retail Properties (ticker “NNN”). According to my projections, real returns for REITs are likely to be an abysmal -3.25% per year in the new decade. This is almost as bad as stocks.

I do realize that real estate is a very diverse asset class and that a couple REITs, regardless of how well chosen, can’t possibly represent every niche. So if you happen to own rental properties far from the overpriced U.S. coastal markets that are cash-flowing nicely, then you might very well be justified in ignoring my real estate return forecast. Just don’t expect to buy a convenient REIT security in your IRA or 401-k account and walk away with positive real returns after inflation.

The situation improves a bit with cash. This asset class should return an uninspiring -0.43% per annum after inflation through the 2020s. And although real returns on cash might be better than what you’ll get in stocks or real estate, they still aren’t positive.

The real return on cash is derived from the 3-month Treasury bill interest rate (1.57%) minus the assumed future rate of inflation (2.0%). Of course, that assessment relies on 3-month Treasury bill rates staying where they are right now. And that, in turn, is a function of what the Federal Reserve decides to do with interest rates. And the open secret there is that the Fed will only drop short-term interest rates in the future.

So that nice safe -0.43% annualized real return actually has downside risk! Of course, cash is nice because it can allow you to pick up investment bargains on the cheap later. But you’ll bleed purchasing power little by little until that day finally arrives.

Next up is corporate bonds, which are represented by the S&P 500 Bond Index. This is a fixed-income index composed of over 5,400 securities issued exclusively by S&P 500 companies. Right now the yield-to-maturity on this index is 2.87%. Subtract inflation from this and you end up with 0.87%.

But that isn’t the end of the story. You also have to account for default risk.

Unfortunately, corporate America has levered itself to the moon since the last financial crisis, increasing its aggregate debt load from $6.3 trillion in 2007 to $10.1 trillion in 2019. As a result, default risks have increased dramatically (although you wouldn’t know it from watching CNBC).

Photo Credit: FRED

In light of these facts, I applied a rather modest 1.1% default rate to the S&P 500 Bond Index, bringing the expected real returns on corporate debt down to -0.23% per annum. In other words, corporate bonds will probably lose you money over the next decade after accounting for inflation.

The next stop on our whirlwind tour of future asset class returns is treasury securities. These ultra-safe bonds are backed by the full faith and credit of the U.S. Government.

However, because they are ultra-safe, you can’t expect to get rich from them. This is reflected in their real returns, which are currently negative. The 10-year Treasury Note trades with a yield-to-maturity of 1.88%, giving a paltry annualized real return of -0.12% over the next 10 years. This is not the stuff that investor’s dreams are made of.

The last asset class I wanted to examine is TIPS, or Treasury Inflation-Protected Securities. These are U.S. Government securities that earn a guaranteed real return that is then adjusted (upward) for inflation. That means that if you hold a TIPS bond until maturity, you will always get a positive real return (assuming its real interest rate was above zero when you purchased it).

TIPS is the only asset class that currently has a positive real return, making it unique among conventional paper assets. Of course, the 10-year TIPS note is only priced to yield 0.15%. But hey, at least it’s positive!

Investment returns this low are just depressing; they make building wealth almost impossible.

But there is an alternative for the sophisticated investor: tangible assets. I’m talking about things like gold and silver bullion, antiques, gemstones and fine art. These are the assets that have been ignored in our crazy, over-the-top “Everything Bubble”.

Now I can’t accurately predict the future returns of tangible assets with any degree of precision, which is why I haven’t included them in the chart above. Antiques and other tangibles are difficult to value because they don’t have cashflows like stocks (dividends) or bonds (interest payments). So you can’t apply traditional valuation metrics, like discounted cashflow analysis or net present value calculations. This is, incidentally, one of the reasons that Wall Street tends to ignore this asset class.

But I can tell you that antiques, gold, fine art, silver and gemstones are all ridiculously undervalued right now. They have simply been forgotten in our collective rush to find the next Amazon, Uber or Google. In addition, tangible assets have no risk of default – an investment attribute that will become increasingly attractive once our current securities market mania collapses in tears.

So while I don’t know exactly what the real returns on antiques and other tangibles might be in the 2020s, I can confidently say that they’ll easily beat all of the 6 conventional asset classes that I’ve outlined in this article. A nominal return of 4% or 5% per annum should be easily achievable. This translates into real returns that are at least 500 basis points higher than anything the stock market casino can muster and a full 200 to 300 basis points better than bonds of even the highest credit quality.

Investors who want to play it safe can buy gold and silver bullion. Those who are more adventurous can load up on antiques like vintage Must de Cartier wristwatches, World War II era U.S. military insignia or Japanese Edo era samurai sword fittings. The sky is the limit for the savvy connoisseur.

Just don’t keep your money in conventional paper assets thinking that it will make you rich.

Read more thought-provoking Antique Sage investing articles here.

-or-

Read in-depth Antique Sage investment guides here.